Pakistan's present economic conditions are unfavorable, to say the least, with a deteriorating external and internal economic environment having plagued the country for over a year. Under such circumstances, it would have been expected that businesses would be in dire straits.

However, contrary to expectations, some of the largest Pakistani entities were able to turn around and report record corporate profits.

Despite economic challenges, Pakistani listed companies reported strong earnings growth in the third quarter of fiscal year 2023. According to a report by Topline Securities, earnings grew by 37% quarter on quarter (QoQ) to Rs. 352 billion, which is contrary to market expectations. The increase in profitability was largely led by the Oil & Gas Exploration (E&P), Banks, and Oil Marketing Companies. However, excluding these three sectors, the profitability remained flat for 3QFY23.

The only sectors to report losses in 3QFY23 were the Automobile and Power sectors. On a year-on-year (YoY) basis, KSE index companies' profitability grew by 15% (-22% YoY in US$), leading 9MFY23 earnings growth to 8% YoY (-21% YoY in US$), with E&Ps, Banks, and Technology leading the way.

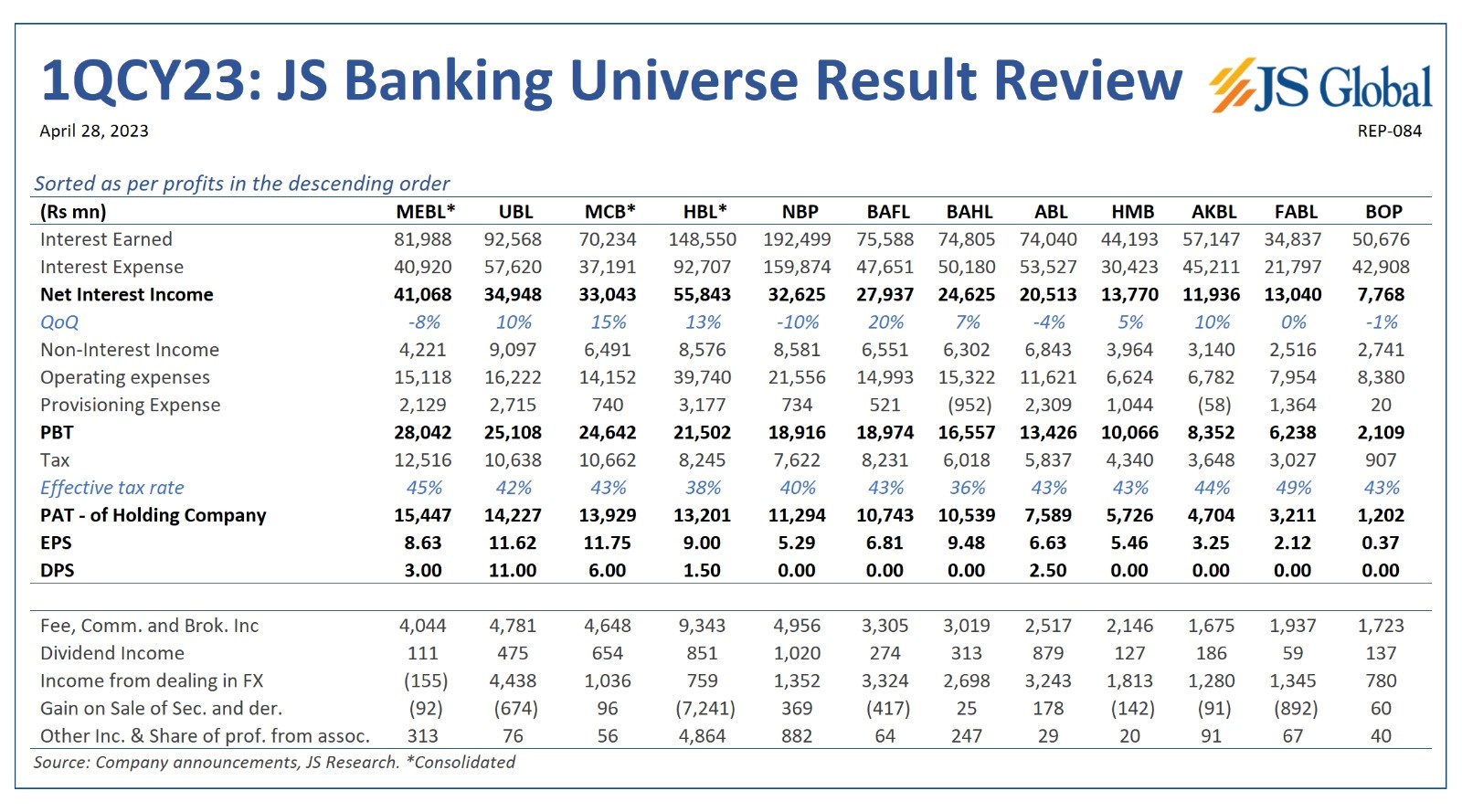

One interesting and somewhat expected member of the group of companies reporting strong earnings were the commercial banks sector. As per the Topline report, commercial banks emerged as the second-best performing sector during 3QFY23, with earnings increasing significantly by 53% YoY and 25% QoQ to Rs. 121 billion for those that are in the KSE100 index. The jump in profitability can be attributed to higher Net Interest Income (NII) resulting from high-interest rates, lower provisions, and higher FX income. Major players, including Bank Alfalah, Bank AL Habib, Habib Bank, Meezan Bank, and Habib Metropolitan, witnessed significant growth, ranging from 60% YoY to Rs. 5.7 billion to 114% YoY to Rs. 10.7 billion. On the other hand, the Bank of Punjab reported a decline of 44% YoY to Rs. 1.2 billion.

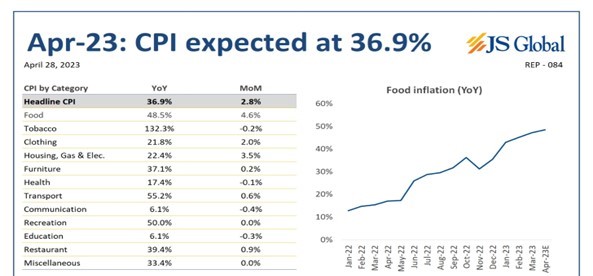

Results for quarter from January to March 2023

The banking sector has experienced significant growth in recent times, largely due to the substantial increase in interest rates. In just a year and a half, the policy rate has tripled and currently stands at 21%. Moreover, with almost three-quarters of banking deposits being directed towards government securities, banks are able to earn substantial profits with minimal risk. However, the government has implemented a supertax that has increased the banking sector taxation to 49%, allowing them to capture a significant portion of the industry's profitability.

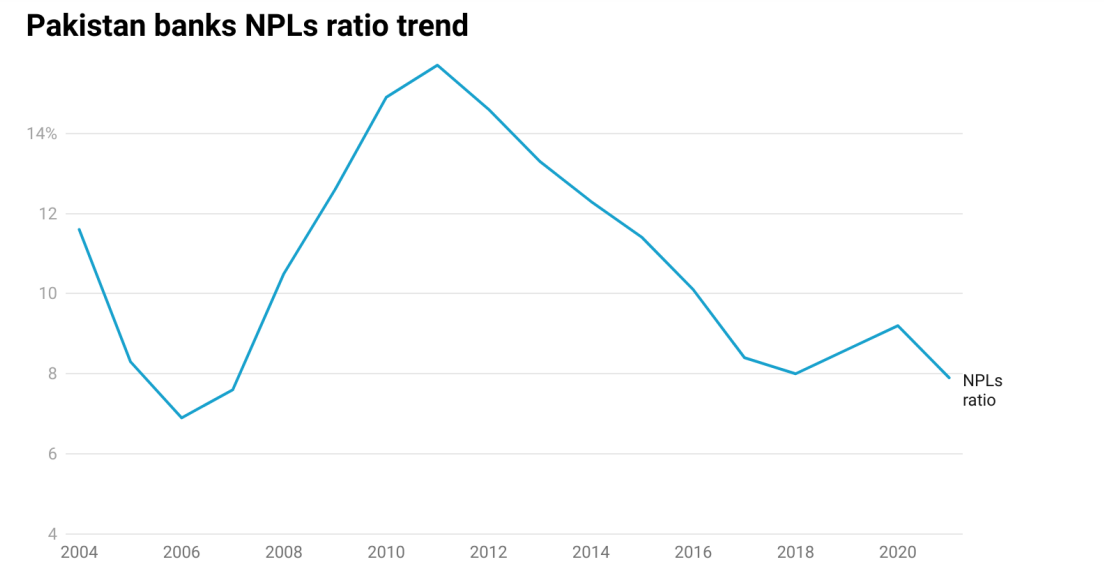

Yet, the profitability run for Pakistani banks might face potential disruption from a rise in Non-Performing Loans (NPLs), commonly referred to as "Bad Loans." In the last decade, Pakistani banks have made significant progress towards improving loan quality. However, macroeconomic challenges, both domestically and globally, pose a threat to this trend.

Nevertheless, the banks remain well-positioned to avoid a build-up of NPLs, thanks to their conservative lending practices and robust capital buffers. The textile sector, which has the highest exposure for most banks, is among the various sectors suffering, and this could trigger a new wave of delinquencies. Despite this, Pakistani banks' prudent approach to lending over the last decade and their low loan-to-deposits ratios serve as protective measures.

Further, the risk of uncertain global economic conditions and recent banking failures, such as SVB, to Pakistan's banking sector is minimal. This is because the industry is primarily funded domestically, with minimal external flows. “Bank capital adequacy ratios are generally healthy across Asia and the region's major banks are largely funded through domestic deposits, mitigating external financing risks. Yet, while the systemic risk is low, there will be areas of vulnerability. More globally integrated lenders reliant on external funding will be the first to feel the effects of current market volatility,” read a report by Economist Intelligence Unit (EIU).

However, what is causing sleepless nights for many bankers are the discussions around domestic debt restructuring. Pakistan's banking sector has approximately half of its assets in government-linked ventures, which is more than eight times their equity. With central bank borrowings prohibited and banking liquidity being squeezed, the government's finances are facing strain. In the event of a drastic sovereign debt restructuring, Pakistani banks may not be able to absorb a substantial haircut due to limited capacity.

As per a recent editorial published by the Business Recorder, “Any big hike would certainly make many businesses default on loans. And the government’s real issue is debt servicing with over 80 percent of government domestic debt linked to short-term rates (be it T-Bills or PIBs floaters). The government is already paying more in debt servicing than its net fiscal revenue. Any increase in rates to exacerbate the problem would increase the chances of domestic debt restructuring, which could be a nightmare.”

Despite the challenges mentioned earlier, Pakistani banks are in a good position to maintain their profitability and continue to benefit from their conservative lending practices in the coming years.

Source: Tellimer

Source: Tellimer