During a recent meeting of the National Assembly's standing committee on finance, Dr. Inayat Hussain, the Deputy Governor of the State Bank of Pakistan (SBP), shared that nearly $3 billion in concessional loans were distributed to approximately 600 borrowers during the PTI government's tenure. While this news may come as a surprise to some, the controversial nature of the Temporary Economic Refinance Facility (TERF), through which the loans were issued by commercial banks, has been widely discussed and documented. The pitfalls of this scheme have been a topic of much debate.

What is TERF and why was it offered?

The TERF was designed to provide concessionary loans to encourage investment in new projects and the Balancing, Modernization, and Replacement (BMR) of existing projects. To qualify for TERF, borrowers had to purchase new imported or locally manufactured plants and machinery for setting up new projects or for BMR or expansion of existing projects.

The 10-year loan facility charges borrowers an annual interest rate of 5%, with 1% allocated to the SBP and the remaining 4% attributed to the spread charged by the commercial bank disbursing the loan. This sounds like a great concessional deal compared to the current policy rate of 21%.

TERF was introduced by the PTI government during the pandemic to provide support to businesses amidst uncertain economic conditions. The scheme aimed to alleviate the unprecedented challenges faced by businesses by encouraging investment in new projects and the modernization of existing ones through concessionary refinance. Its goal was to provide respite to businesses and stimulate economic activity.

Heart in the right place, but not in the scheme

One of the many ills of this scheme, as argued by economist Ammar Habib, was that by design it supported large industrial units, which limited the number of beneficiaries to a few hundred industrialists and capital owners who received a subsidized interest rate.

Ammar also states in his article that the subsequent surge in investment drove up the demand for imported machinery and resulted in a current account deficit as the central bank pursued an expansionary monetary policy for too long. Resultantly, liquidity risks surfaced, and importing equipment became more challenging, causing cost overruns and delays in commercial operations.

This, however, also added to the exceptional growth that the country experienced after Covid. “Post-Coivd, Pakistan’s economy grew at a rate of almost 6% for 2 years. Unfortunately, due to the nature of our economy, such high growth spells lead to the economy’s overheating. Therefore, now the growth has to be slowed down to manage the current account deficit,” former SBP, Chief Murtaza Syed stated in a podcast.

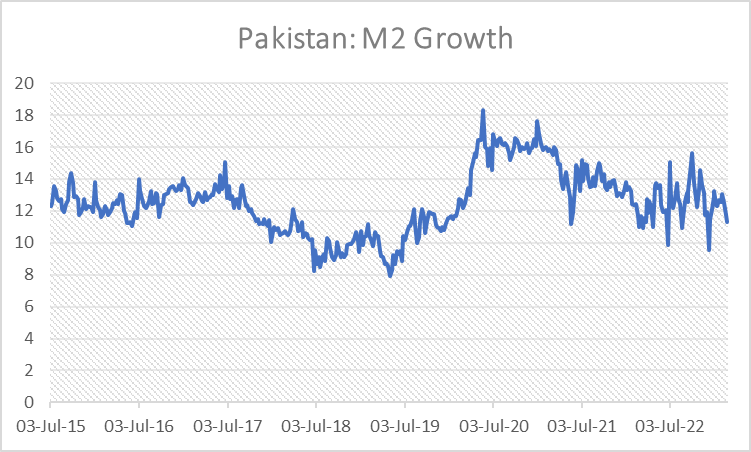

Further, by introducing such schemes, SBP injected exceptional amounts of liquidity into the system which have a medium to long-term inflationary impact. The graph above clearly depicts a surge in the money supply during 2020.

DMKM's substack provides a skillful explanation of the concept of how money is created through such schemes. It explains that the central bank much like commercial banks can create money by lending. In this case, SBP is creating money by crediting reserve accounts of commercial banks that disburse TERF loans.

In double-entry accounting, the central bank adds loan balances to the commercial bank loans asset account and increases the commercial bank’s deposits/reserves on the liability side of its balance sheet. This is exemplified through the refinance loan, where the commercial bank reflects the loan as borrowing on their liability side and replicates it as an export refinance loan to the exporter on their asset side. Subsequently, if an exporter that has borrowed through HBL pays a supplier who banks with UBL, HBL can transfer the newly credited SBP reserves to UBL's account at SBP. Thus, effectively adding liquidity to the whole system.

Therefore, the burden of such subsidies is footed by the SBP instead of the government which creates distortions through understating the fiscal deficit. “We see that a clear dividing line between SBP operations and the refinancing schemes is imperative on governance grounds, allowing SBP to focus on its core objectives. Such a structural change will allow support to the export sector transparently through an on-budget subsidy. In this regard, the Ministry of Finance and SBP have advanced work on an initial plan in consultation with other stakeholders to establish an appropriate Development Finance Institution to support the eventual phasing out of the refinance facilities,” read the IMF Staff report published in September 2022.

Therefore, the burden of such subsidies is footed by the SBP instead of the government which creates distortions through understating the fiscal deficit. “We see that a clear dividing line between SBP operations and the refinancing schemes is imperative on governance grounds, allowing SBP to focus on its core objectives. Such a structural change will allow support to the export sector transparently through an on-budget subsidy. In this regard, the Ministry of Finance and SBP have advanced work on an initial plan in consultation with other stakeholders to establish an appropriate Development Finance Institution to support the eventual phasing out of the refinance facilities,” read the IMF Staff report published in September 2022.

Yet, one of the most undesirable but imminent outcomes of such schemes is blatant abuse by those in a position of power by earmarking funds for personal investments.

https://twitter.com/YousufNazar/status/1644695096103784448

“Criticizing the lopsided distribution of subsidized loans under the Temporary Economic Refinance Facility (TERF), Finance Minister Miftah Ismail said that only one individual received as much as Rs 90 billion through the concessionary refinance scheme,” reported DAWN on September 3, 2022.

Despite being part of a list of poorly conceived government schemes in the last tenure that included the Naya Pakistan Housing and Kamyab Pakistan Program, TERF was a genuine attempt to weather the economic headwinds brought on by the pandemic. While the scheme may yield dividends in the future by enhancing export capacity, the jury is still out on the distributional impacts of the state providing low-interest rate financing, that effectively serves as a subsidy to TERF recipients in today’s high interest rate monetary landscape.

What is TERF and why was it offered?

The TERF was designed to provide concessionary loans to encourage investment in new projects and the Balancing, Modernization, and Replacement (BMR) of existing projects. To qualify for TERF, borrowers had to purchase new imported or locally manufactured plants and machinery for setting up new projects or for BMR or expansion of existing projects.

The 10-year loan facility charges borrowers an annual interest rate of 5%, with 1% allocated to the SBP and the remaining 4% attributed to the spread charged by the commercial bank disbursing the loan. This sounds like a great concessional deal compared to the current policy rate of 21%.

TERF was introduced by the PTI government during the pandemic to provide support to businesses amidst uncertain economic conditions. The scheme aimed to alleviate the unprecedented challenges faced by businesses by encouraging investment in new projects and the modernization of existing ones through concessionary refinance. Its goal was to provide respite to businesses and stimulate economic activity.

Heart in the right place, but not in the scheme

One of the many ills of this scheme, as argued by economist Ammar Habib, was that by design it supported large industrial units, which limited the number of beneficiaries to a few hundred industrialists and capital owners who received a subsidized interest rate.

Ammar also states in his article that the subsequent surge in investment drove up the demand for imported machinery and resulted in a current account deficit as the central bank pursued an expansionary monetary policy for too long. Resultantly, liquidity risks surfaced, and importing equipment became more challenging, causing cost overruns and delays in commercial operations.

This, however, also added to the exceptional growth that the country experienced after Covid. “Post-Coivd, Pakistan’s economy grew at a rate of almost 6% for 2 years. Unfortunately, due to the nature of our economy, such high growth spells lead to the economy’s overheating. Therefore, now the growth has to be slowed down to manage the current account deficit,” former SBP, Chief Murtaza Syed stated in a podcast.

tweeted by Dr. Ahmed Jamal Pirzada

Further, by introducing such schemes, SBP injected exceptional amounts of liquidity into the system which have a medium to long-term inflationary impact. The graph above clearly depicts a surge in the money supply during 2020.

DMKM's substack provides a skillful explanation of the concept of how money is created through such schemes. It explains that the central bank much like commercial banks can create money by lending. In this case, SBP is creating money by crediting reserve accounts of commercial banks that disburse TERF loans.

In double-entry accounting, the central bank adds loan balances to the commercial bank loans asset account and increases the commercial bank’s deposits/reserves on the liability side of its balance sheet. This is exemplified through the refinance loan, where the commercial bank reflects the loan as borrowing on their liability side and replicates it as an export refinance loan to the exporter on their asset side. Subsequently, if an exporter that has borrowed through HBL pays a supplier who banks with UBL, HBL can transfer the newly credited SBP reserves to UBL's account at SBP. Thus, effectively adding liquidity to the whole system.

Therefore, the burden of such subsidies is footed by the SBP instead of the government which creates distortions through understating the fiscal deficit. “We see that a clear dividing line between SBP operations and the refinancing schemes is imperative on governance grounds, allowing SBP to focus on its core objectives. Such a structural change will allow support to the export sector transparently through an on-budget subsidy. In this regard, the Ministry of Finance and SBP have advanced work on an initial plan in consultation with other stakeholders to establish an appropriate Development Finance Institution to support the eventual phasing out of the refinance facilities,” read the IMF Staff report published in September 2022.Yet, one of the most undesirable but imminent outcomes of such schemes is blatant abuse by those in a position of power by earmarking funds for personal investments.

https://twitter.com/YousufNazar/status/1644695096103784448

“Criticizing the lopsided distribution of subsidized loans under the Temporary Economic Refinance Facility (TERF), Finance Minister Miftah Ismail said that only one individual received as much as Rs 90 billion through the concessionary refinance scheme,” reported DAWN on September 3, 2022.

Despite being part of a list of poorly conceived government schemes in the last tenure that included the Naya Pakistan Housing and Kamyab Pakistan Program, TERF was a genuine attempt to weather the economic headwinds brought on by the pandemic. While the scheme may yield dividends in the future by enhancing export capacity, the jury is still out on the distributional impacts of the state providing low-interest rate financing, that effectively serves as a subsidy to TERF recipients in today’s high interest rate monetary landscape.