The US regulators have taken over Silicon Valley Bank (SVB), which primarily served tech startups. The bank had over $200bn in assets and $170bn in deposits. SVB’s precarious position has led to a massive run on its deposits, making it the largest banking collapse since the 2008 banking crisis.

“Based in Santa Clara, the lender was ranked as the 16th biggest in the U.S. at the end of last year, with about $209 billion in assets. Specifics of the tech-focused bank's abrupt collapse were a jumble, but the Fed's aggressive interest rate hikes in the last year, which had crimped financial conditions in the start-up space in which it was a notable player, seemed front and center,” Reuters reported.

The Catalyst Of Disaster

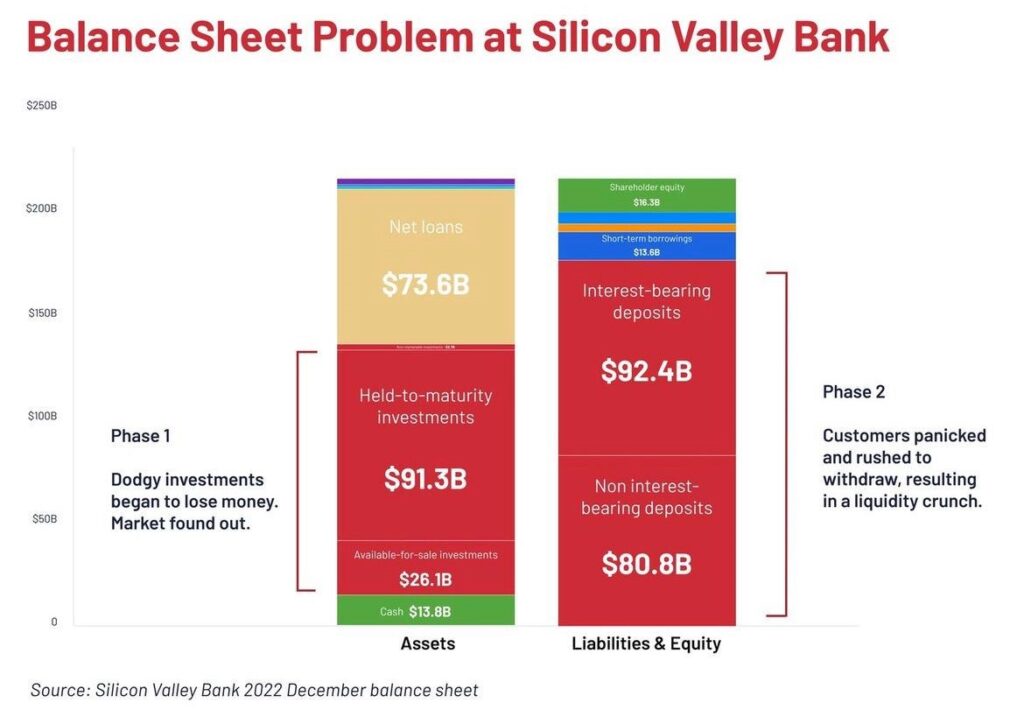

SVB had invested $91bn of deposits in long-term US treasuries before the monetary tightening cycle (interest rate hikes) began, resulting in an estimated $15 billion drop in bond values.

To cover withdrawals of deposits by some tech companies (as funds in the tech ecosystem dried up), SVB was forced to sell their bond holdings, incurring about 1.8 billion in losses. Though the US regulator assured that the depositors will have access to their insured deposits by March 13, 85 percent of the bank's deposits are uninsured, with most accounts in excess of the $250,000 insurance cap. This will affect customers’ (tech startups) operations and even their ability to pay their employees.

Source: Rehab Mohsin

The problems for SVB started when the US tech startup space was pumped with billions of dollars of cheap money and the bank accumulated large amounts of deposits from its clientele.

“US venture capital-backed companies raised $330 billion in 2021 — almost doubling the previous record a year before,” read an article in Bloomberg.

“Crucially, the Federal Reserve pinned interest rates at unprecedented lows. And, in a radical shakeup of its framework, it promised to keep them there until it saw sustained inflation well above 2% — an outcome that no official forecast. SVB took in tens of billions of dollars from its venture capital clients and then, confident that rates would stay steady, ploughed that cash into longer-term bonds,” the Bloomberg article further added.

The bank, therefore, parked around $91 billion of those funds in US treasuries (long-term bonds) in 2021. But why would they do that?

Basically, banks maintain a fractional reserve of their funds to honour withdrawal requests from customers. The system works under the assumption that not all depositors would require to withdraw their total funds at once. Therefore, the excess funds are then invested or lent to borrowers. This way banks are able to earn profits on the rate differential between the amounts they pay their depositors and the returns generated from lending/investing.

However, as the interest rate picked up and economic activity slowed down, the venture capital (VC) money started drying out and the bank’s major depositors, tech startups, started drawing on their reserves to finance operations.

Yet, the question remains. How come the bank ended up taking huge losses on its bonds when it was placed with the US government which essentially is the most secure place to invest?

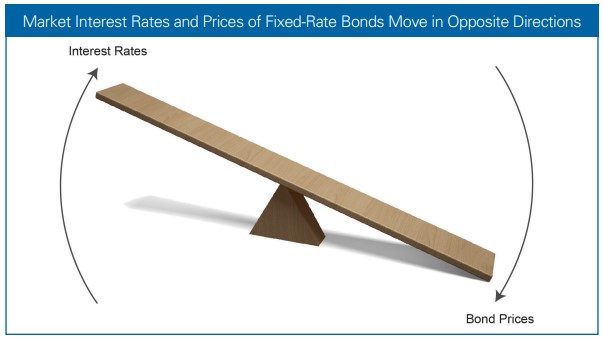

The answer to this is in how the bonds actually work. “A fundamental principle of bond investing is that market interest rates and bond prices generally move in opposite directions. When market interest rates rise, prices of fixed-rate bonds fall. This phenomenon is known as interest rate risk,” read an investor bulletin by US Securities and Exchange Commission (SEC).

Source: SEC

Yet, this loss could have been averted if the bonds were held by SVB till maturity, as unlike stocks, bonds have a maturity date at which the invested amount needs to be paid back. Unfortunately, a looming threat of rating downgrade from Moody’s led SVB to sell off the investments and book a loss.

https://twitter.com/theantonioreza/status/1634143128419459073?t=WmeYH0I3vY9SPLhtV7GyFA&s=09

“If you intend to hold a bond to maturity, the day-to-day fluctuations in the bond’s price may not be as important to you. The bond’s price may change, but you will be paid the stated interest rate, as well as the face value of the bond, upon maturity,” the SEC bulletin further added.

Therefore, this ignited a series of events which led to a run on the bank.

Will Pakistani Banks Have A Similar Fate?

Pakistani banks aren’t immune to the mechanics of the bond market. Further, they have a significant exposure in government securities. Therefore, when the State Bank of Pakistan (SBP) began the rate hikes last years, the banks’ concerns around accumulating losses grew and they asked the SBP for a reclassification of the investments in their books. However, unlike SVB, they had the luxury to wait for the bonds to mature and not book a loss. The local banks are well capitalised with a diverse solid retail depositors base.

Yet, undercapitalised banks are still present in the system threatening public’s confidence. “The government has committed to the IMF that Summit Bank and Silkbank will be sent into “resolution” by May 2023 if they don’t complete the first stage of their recapitalisation plan by March of the same year. If this happens, these banks could be the next to be forcibly restructured or even sold off altogether like KASB Bank was in 2015,” Khurram Husain, Senior Business Journalist, wrote in an article for Profit.

Another Global Financial Crisis?

The impact of SVB’s collapse will unfold in the coming days. However, as per experts, the impact of this, unlike the 2008 global financial crisis, would not be a widespread one as over the past decade and a half, regulations have been tightened to keep a check on the banking sector.

“Based in Santa Clara, the lender was ranked as the 16th biggest in the U.S. at the end of last year, with about $209 billion in assets. Specifics of the tech-focused bank's abrupt collapse were a jumble, but the Fed's aggressive interest rate hikes in the last year, which had crimped financial conditions in the start-up space in which it was a notable player, seemed front and center,” Reuters reported.

The Catalyst Of Disaster

SVB had invested $91bn of deposits in long-term US treasuries before the monetary tightening cycle (interest rate hikes) began, resulting in an estimated $15 billion drop in bond values.

To cover withdrawals of deposits by some tech companies (as funds in the tech ecosystem dried up), SVB was forced to sell their bond holdings, incurring about 1.8 billion in losses. Though the US regulator assured that the depositors will have access to their insured deposits by March 13, 85 percent of the bank's deposits are uninsured, with most accounts in excess of the $250,000 insurance cap. This will affect customers’ (tech startups) operations and even their ability to pay their employees.

Source: Rehab Mohsin

The problems for SVB started when the US tech startup space was pumped with billions of dollars of cheap money and the bank accumulated large amounts of deposits from its clientele.

“US venture capital-backed companies raised $330 billion in 2021 — almost doubling the previous record a year before,” read an article in Bloomberg.

“Crucially, the Federal Reserve pinned interest rates at unprecedented lows. And, in a radical shakeup of its framework, it promised to keep them there until it saw sustained inflation well above 2% — an outcome that no official forecast. SVB took in tens of billions of dollars from its venture capital clients and then, confident that rates would stay steady, ploughed that cash into longer-term bonds,” the Bloomberg article further added.

The bank, therefore, parked around $91 billion of those funds in US treasuries (long-term bonds) in 2021. But why would they do that?

Basically, banks maintain a fractional reserve of their funds to honour withdrawal requests from customers. The system works under the assumption that not all depositors would require to withdraw their total funds at once. Therefore, the excess funds are then invested or lent to borrowers. This way banks are able to earn profits on the rate differential between the amounts they pay their depositors and the returns generated from lending/investing.

However, as the interest rate picked up and economic activity slowed down, the venture capital (VC) money started drying out and the bank’s major depositors, tech startups, started drawing on their reserves to finance operations.

Yet, the question remains. How come the bank ended up taking huge losses on its bonds when it was placed with the US government which essentially is the most secure place to invest?

The answer to this is in how the bonds actually work. “A fundamental principle of bond investing is that market interest rates and bond prices generally move in opposite directions. When market interest rates rise, prices of fixed-rate bonds fall. This phenomenon is known as interest rate risk,” read an investor bulletin by US Securities and Exchange Commission (SEC).

Source: SEC

Yet, this loss could have been averted if the bonds were held by SVB till maturity, as unlike stocks, bonds have a maturity date at which the invested amount needs to be paid back. Unfortunately, a looming threat of rating downgrade from Moody’s led SVB to sell off the investments and book a loss.

https://twitter.com/theantonioreza/status/1634143128419459073?t=WmeYH0I3vY9SPLhtV7GyFA&s=09

“If you intend to hold a bond to maturity, the day-to-day fluctuations in the bond’s price may not be as important to you. The bond’s price may change, but you will be paid the stated interest rate, as well as the face value of the bond, upon maturity,” the SEC bulletin further added.

Therefore, this ignited a series of events which led to a run on the bank.

Will Pakistani Banks Have A Similar Fate?

Pakistani banks aren’t immune to the mechanics of the bond market. Further, they have a significant exposure in government securities. Therefore, when the State Bank of Pakistan (SBP) began the rate hikes last years, the banks’ concerns around accumulating losses grew and they asked the SBP for a reclassification of the investments in their books. However, unlike SVB, they had the luxury to wait for the bonds to mature and not book a loss. The local banks are well capitalised with a diverse solid retail depositors base.

Yet, undercapitalised banks are still present in the system threatening public’s confidence. “The government has committed to the IMF that Summit Bank and Silkbank will be sent into “resolution” by May 2023 if they don’t complete the first stage of their recapitalisation plan by March of the same year. If this happens, these banks could be the next to be forcibly restructured or even sold off altogether like KASB Bank was in 2015,” Khurram Husain, Senior Business Journalist, wrote in an article for Profit.

Another Global Financial Crisis?

The impact of SVB’s collapse will unfold in the coming days. However, as per experts, the impact of this, unlike the 2008 global financial crisis, would not be a widespread one as over the past decade and a half, regulations have been tightened to keep a check on the banking sector.