A standard undergraduate Microeco-nomics course will tell you what factors influence the exchange rate. The prime one is of course the balance of payments itself – a current account that is perpetually in deficit is going to cause a depreciation in the value of the currency. The other major factor is inflation – or more specifically, domestic inflation in comparison to inflation in your closest trading partner countries. In simple terms, if inflation in your country is higher than in your trading partners, your currency is going to depreciate relative to theirs.

There are other factors too, which mainly apply to countries which experience a higher level of capital flows than Pakistan typically does. Thus if you experience a rush of foreign investment in your sovereign bonds, your currency will appreciate in value and vice versa. The same is true if there are other forms of inflows in your capital account. This last factor can cause a lot of volatility in the exchange rate. In other words, if what you are experiencing is “hot money” inflows or outflows, your exchange rate, relative to most international currencies, will go up or down depending on how often and how much international currency flows into or out of your capital account.

[quote]Three months on, the Finance Minister's seemingly bizarre statement makes sense[/quote]

Sometime around December 2013, the Finance Minister made a rather belligerent statement addressing those who want to “dollarize” the economy, keep savings in dollars, and resist remitting export receipts. The gist of his statement was that the rupee would soon appreciate against the dollar, and dollar deposits would not be as good a store of value as one would suppose. The confidence with which this statement was made, at a time when the value of the rupee had slid to about Rs 108 to a dollar, should have raised questions, not least because the government didn’t seem to be doing much about improving the current account deficit or controlling inflation.

Three months on, the Finance Minister’s seemingly bizarre statement makes sense. While foreign exchange reserves (held with the State Bank) were not rising much above $3.5 billion, the current account deficit was still close to half a billion dollars (and about half a percent of GDP), and inflation was still close to 9 percent as it had been since the beginning of the fiscal year, the government was keeping busy negotiating a bailout with friendly Arab countries. Within a week in early March, the rupee appreciated by 6 percent – unprecedented in the recent history of currency trading in Pakistan. On March 1, the rupee was trading at 104 to a dollar, while on March 12, it had dropped to about 98.

[quote]There are only so many calls for regime change that Pakistan can make, and only so many pipeline deals that can be called off[/quote]

What else was happening that week? There was Pakistan’s about-turn on Syria, including demands for regime change in a country which has no history of commenting on Pakistan’s internal affairs, and the government’s determination to hold talks with a TTP which can’t seem to control its splinter groups. Next thing we know, Saudi Arabia has “donated” $1.5 billion to us, the monies having being deposited in a special fund called the “Pakistan Development Fund” to be used for, among other things, building a Motorway linking Sindh to the central and north Punjab. Another $1.5 billion is expected to materialize in this fund in another few weeks, “donated” by the UAE (or perhaps by Saudi Arabia – not much is clear at this point). This in addition to the release of $550 million in Coalition Support Funds, and the expected release of the next IMF tranche, also about $550 million, by end March. If the 3G auction goes through in early April, and privatization picks up before the end of the fiscal year, the government will be flush.

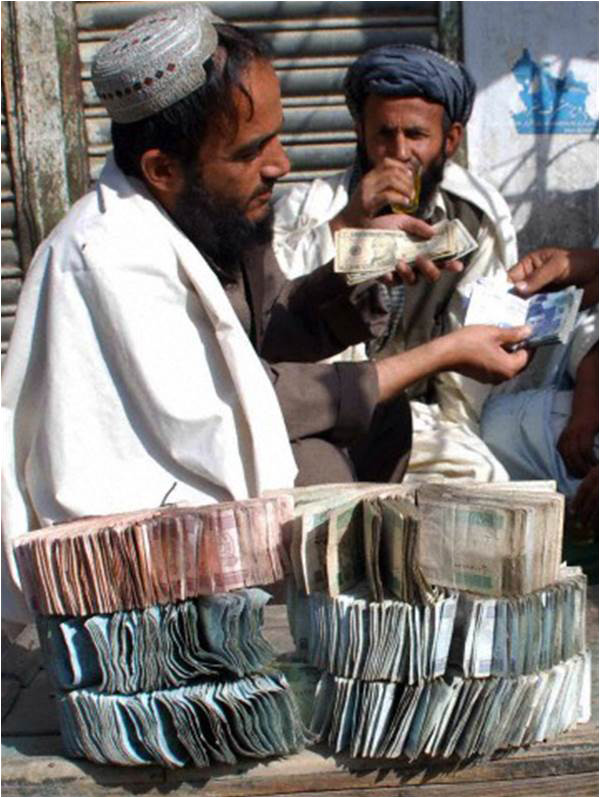

Currency exchange dealers trade Pakistani rupees and US dollars on a roadside near the Afghan border in Chaman

This should be good news, but somehow, elation is not what many analysts are feeling at the moment. Key macro indicators had shown improvement in this third quarter of the fiscal year, but not enough to merit such a significant currency appreciation. The CSF payment was a relief, but was long overdue. The IMF tranche was expected. The government’s policy of making payments for oil imports through commercial loans and not by mopping up dollars in the market had indeed released some pressure on the rupee, but the loans are still a liability. Market sentiments are up due to the expectation of the telecom auctions actually going ahead and key privatization deals going forward, but market sentiments do not usually cause the exchange rate to shoot by over 6 percent in a few days. The key factor in the appreciation over a period of just a few days was undoubtedly the flow of funds from Saudi Arabia.

The Finance Minister claims that this is not a loan, but a “gift.” A bilateral grant of $1.5 billion (or $3 billion if the next tranche materializes in the next few weeks as expected) is practically unheard of in this day and age. The prominent recent example of such generosity is from Cuba and Venezuela where the latter provides oil to the former in exchange for medical expertise, and training in the use of Soviet made military equipment. Even there, where the two governments are closely bound by a common ideology and the need to stave off a joint powerful enemy in the form of the US, the exchange is not a free lunch for either. Yet we are supposed to believe that an increasingly jittery Saudi Arabia, which is nervously watching a strengthening of Iranian influence in its neighborhood and possible rapprochement between Iran and the US internationally, is displaying generosity towards us purely on the basis of brotherly sentiment and a fondness for Mr Nawaz Sharif? Would that it were so, but it’s all a bit difficult to believe.

In any event, it would be foolish to further delay crucial economic reform in the face of a sudden rush of foreign aid inflows. There are only so many calls for regime change that Pakistan can make, and only so many pipeline deals that can be called off.