The Pakistani government is gearing up to present the federal budget for the fiscal year 2024, with a focus on debt servicing due to current economic concerns. To address the significant expenses, the government has set an ambitious target of Rs 9.2 trillion in tax revenue for FY24, representing a 20% YoY growth from the FY23 budget. However, there has been some volatility leading up to the budget presentation.

Recently, Prime Minister Shehbaz Sharif contacted IMF Managing Director Kristalina Georgieva to revive the $6.5 billion bailout package. Just two days after the PM established contact, the IMF Mission Chief to Pakistan, Nathan Porter, expressed concern about the political uncertainty in the country. This statement drew criticism from government officials, with Minister of State for Finance Aisha Ghaus Pasha lashing out at the Fund for meddling in Pakistan's internal matters. She also indicated that the government has a “Plan B” in case the IMF deal does not materialize.

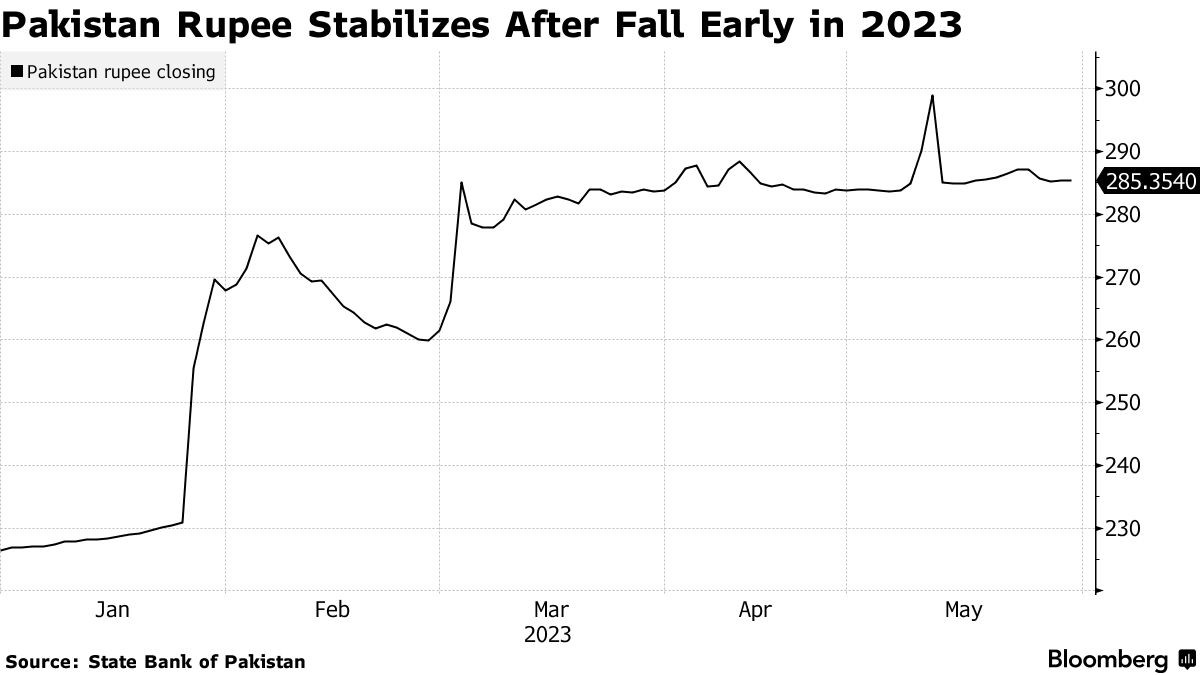

The Fund, amongst other things, has asked the country to fix the currency market and close the gap between the interbank and open market rate. “The rupee has slid more than 20% this year after Pakistan officials loosened their control on the currency in January to help secure the IMF loan. The rupee has stabilized since then and traded near 285 rupees per dollar in May. It has seen a gap of almost 8% emerge between the official rate and the one seen at money changers,” reported Bloomberg.

However, a couple of days later the government did manage to close the gap between the two rates by easing demand pressure from the open market and allowing the price of the dollar in retail to come down.

As per Dawn, “the rise in the value of the rupee in the open market came after the State Bank of Pakistan (SBP) allowed banks to acquire US dollars from the interbank market for the settlement of card-based cross-border transactions with the International Payment System.”

Experts have noted that banks are only allowed to carry out these trades until July 31st, 2023, which may present a buying opportunity for money exchangers who could sit on the dollar and wait for the rate to increase again.

Source: Bloomberg News

Meanwhile, the Finance Minister, Ishaq Dar, is adamant that he has everything under control and that Pakistan is out of troubled waters.

However, this view is not shared by many analysts. One of them is Economist Atif Mian. He recently tweeted out a thread criticizing the government’s mismanagement of the economy. He wrote, “The government would rather cut the country's GDP in order to sell cheap petrol. But then lower GDP will make it more difficult to pay off the debt - leading to more devaluation - more misery - and higher petrol prices in terms of purchasing power. This is just one example of the non-sensical policy choices being made addressing a BOP crisis requires that a country acts decisively, restructures aggressively, and takes courageous decisions that demonstrate a clear break from the past.”

However, this time around, the Finance Ministry, uncharacteristically, responded to the Mian’s critique. “The author has completely ignored the deep-rooted reforms Pakistan has undertaken in the last 9 months. These included market exchange rate, interest rate adjustments, mid-year taxation to improve fiscal position, imposition of levy on petroleum products and non- monetization of fiscal deficit,’ read the official rebuttal.

Unfortunately, the reforms being mentioned are not at all deep-rooted, but rather quick fixes to appease the IMF, which has been giving the government a hard time.

Regarding the current situation, is there a contingency plan in place should the primary strategy not work out? Analyst suggests that the focus is currently on preventing a default with the help of bilateral partners, with the aim of postponing a longer-term solution until after the upcoming elections.

Further, the upcoming budget would require the IMF’s stamp of approval if the program is to move forward. As per a report by the Business Recorder, the government is currently considering the possibility of introducing utility subsidies in the upcoming budget. However, this move could lead to a potential strain on an already limited revenue base, which in turn may lead to increased domestic borrowing and negatively affect private-sector borrowing. Raising subsidies without properly targeting them could also limit fiscal space even further. To balance the budget, there may also be a reduction in development budgets, which could result in greater reliance on China for the successful completion of CPEC projects.

While the upcoming budget might end the debate about whether the government is going through with the current IMF program or not, media outlets have started reporting that decision has already been made and the government has given up on the current program and would enter into a new IMF program after the budget.

Though this might be the case, Pakistan still needs to be under the umbrella of an IMF program, as it has massive debt service obligations over the next two fiscal years, and engaging with the Fund means that it has a certain level of leverage to prevent default. Yet, the new program would come with even harsher conditions that are likely to further squeeze the public, which has already been suffering from a 38% record high inflation rate.

It looks like the current officeholders have essentially made up their minds to throw the caretaker setup under the bus.

While the upcoming budget might end the debate about whether the government is going through with the current IMF program or not, media outlets have started reporting that decision has already been made and the government has given up on the current program and would enter into a new IMF program after the budget.

While the upcoming budget might end the debate about whether the government is going through with the current IMF program or not, media outlets have started reporting that decision has already been made and the government has given up on the current program and would enter into a new IMF program after the budget.