Pakistan is finally catching up with the International Monetary Fund’s (IMF) requirement and moving forward with multiple reforms that were demanded by the lender of last resort. The government is increasing gas prices, planning on addressing the circular debt issue through channeling its dividends and gearing up for fiscal measures to achieve revenue targets.

Further, Saudi Arabia and UAE have also come to the country’s aid, days after generous pledges were received by Prime Minister Shehbaz Sharif in Geneva. Therefore, at this pace, the country is likely to be afloat in the near future.

All these recent developments might feel like achievements and give a false sense of relief, but as pessimistic as it sounds, the worst isn’t over yet.

In a recent report, the World Bank lowered Pakistan’s GDP growth forecast for 2023 to two percent, almost half of its earlier estimate.

“In Pakistan, an already precarious economic situation, with low foreign exchange reserves and large fiscal and current account deficits, was exacerbated last August by severe flooding, which cost many lives. About one-third of the country’s land area was affected, damaging infrastructure, and directly affecting about 15 percent of the population. Recovery and reconstruction needs are expected to be 1.6 times the FY2022/23 national development budget,” read the report.

“The flooding is likely to have seriously damaged agricultural production — which accounts for 23 percent of GDP and 37 percent of employment — by disrupting the current and upcoming planting seasons and pushed between 5.8 and 9 million people into poverty. Policy uncertainty further complicates the economic outlook,” It further added.

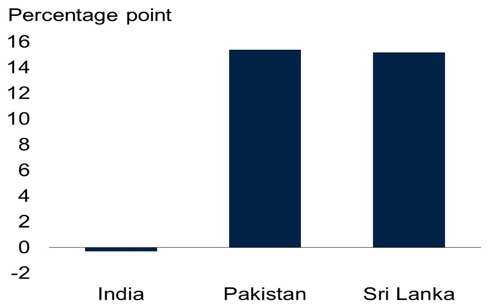

Change In Sovereign Risk Spread Since June 2022

Source: World Bank

The report also indicated that fallout from the Russia-Ukraine war and the end of low interest rate regime across the globe will pose significant threats going forward to many emerging market economies, including Pakistan.

The reduced growth outlook for the country is partially due to its inability to access international financial markets and implement policy measure to reduce balance of payments deficits.

The World Bank report also pointed out other risks that posed a significant threat to economies in the South Asian region, “More persistent high inflation in advanced economies would require additional increases in their policy rates, which could lead to financial stress in the region and further exchange rate pressures. Addressing rising macroeconomic imbalances, which requires fiscal and monetary policy consolidation, is challenging when growth is slowing, and human deprivation is rising. The complexities of such an environment can amplify the risk of policy mistakes that undermine economic activity, especially in circumstances of high domestic debt and dwindling foreign exchange reserves.”

For Pakistan, the risks are amplified due to the state’s inability to manage the chronic current account deficit and create any sort of buffer to fall back on in case of external shocks.

However, there is method to this madness and a very evident one. Behind the perpetual deficit is the fact that the government is the largest borrower from the domestic markets and that money is used for massive spending. This creates excess demand in the economy leading to increased imports which translates into a growing fiscal deficit. Therefore, to cover the deficit, the country is reliant on external borrowing.

On the other side, ideally, the inflows should cover up for the imports, but they remain insufficient as two major avenues, exports and foreign direct investment (FDI), doesn’t achieve their potential because local businesses and products remain an unattractive proposition for international investors and consumers.

A major reason behind it is that the local micro, small and medium-sized enterprises (MSMEs) are deprived of financing which restricts their ability to grow and eventually scale to a level where they can compete internationally.

“Interest rate growth has a direct correlation, perhaps a weak one, with private sector borrowing. As cost of funds increase, we see a push back from the government which is the largest borrower and as result there is room for private sector to access the funds,” said Dr. Ahmed Pirzada in a podcast interview.

The claims are further substantiated by the fact that over the course of past 12 months, the policy rate has grown from 9.75 percent to 16 percent yet there was a considerable growth in private sector financing.

Further, what holds back the private sector from growing and becoming internationally competitive is the fact that those at the helm of affairs and responsible for carrying out the reforms are currently the biggest beneficiaries of the status quo.

“A successful economy keeps giving rise to new entrepreneurs, representing newly emerging industries and technologies, becoming its richest people. But not here in Pakistan where wealth, power and opportunities are strictly limited to an unchanging elite,” wrote, former finance minister, Miftah Ismail in an article for Dawn.

Therefore, what has transpired in the last year or so isn’t something new. The ingredients for disaster were present in our economy’s structure and it was just a matter of time. Experts saw this coming and warned of the consequences.

Economist Uzair Younus, in an article for this publication, back in 2016, wrote, “The government that comes to power after the 2018 elections will run higher budget deficits, leading to increase in the rate of inflation. Large infrastructure and public-sector development programs will have to be cut. And the SBP will be forced to increase interest rates to curb inflation. The ensuing economic slowdown will further constrain the government’s revenue capacity and add to the budgetary woes.”

“Given the rise in external debt, the run on the rupee will be larger than what has been witnessed in prior instances. To stabilize the value of the currency, the PML-N government has allowed it to remain overvalued — the IMF has raised this issue in successive reports. In a crisis where reserves are declining rapidly, the rupee will come under profound pressure, leading to a remarkable depreciation in a short period of time,” he further elaborated.