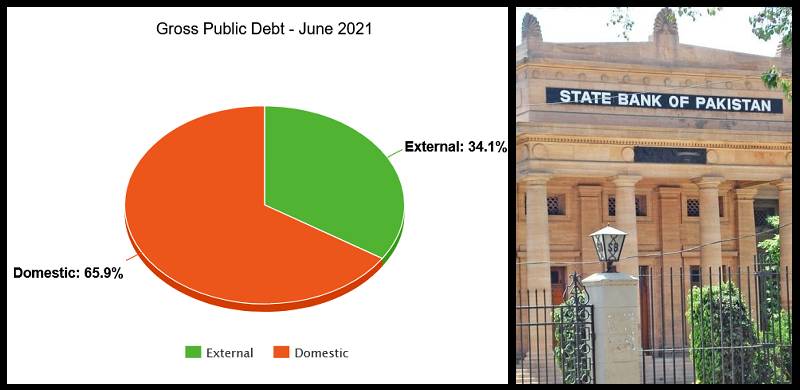

The direction of the State Bank of Pakistan (SBP) to commercial banks regarding the applicability of International Financial Reporting Standards (IFRS-9) in respect of loans, securities and guarantees of the Government of Pakistan has become operative with effect from 01 January, 2022. Since the IFSR-9 initial issuance in 2019, an exemption till 31 December 2021 was given by the SBP to the banks regarding the enforcement of IFRS-9 on the aforesaid classes of sovereign assets. As the SBP has not extended the said exemption to the commercial banks, it essentially means that the Government of Pakistan can default on its Pak Rupee (domestic debt) obligations.

In other words, the SBP has advised the banks to start taking into account the probability of default on sovereign loans taken by the Government and, as a result, to make adequate provision in their financial statements for the potential loss on such sovereign lending.

A belief that the government cannot default on domestic debt has been virtually buried.

Pakistan’s history on sovereign obligations

Since its inception in August 1947, Pakistan has never defaulted on any of its domestic debt/obligations. Furthermore, barring the 1971 separation of East Pakistan, when a small default occurred on Official Bilateral Debt, Pakistan has not ever defaulted on its external debt. With such a long history of performance, it is curious as to why the SBP has chosen to require the banks to make provisions for holding Pak-rupee-denominated credit and securities of the Federal Government.

It is incomprehensible to suggest that the Government of Pakistan, a sovereign state capable of printing its currency, would ever fail to fulfill its Pak-rupee-denominated debt servicing obligations. Therefore, it makes no sense to deprive government loans and securities from the status of “risk-free” sovereign financial assets.

What could the rationale be?

The SBP has not given any rationale for the said change.

The best explanation is the need to enforce IFRS-9. However, given that government loans and securities were exempted until 31 December 2021, there has to be some basis for withdrawal of such exemption.

This is a serious matter and the SBP should have consulted the Government of Pakistan before taking such a far-reaching step.

What are the effects?

The foremost implication of excluding government loans and sovereign securities from the status of “risk-free financial assets” is an increase in the cost of borrowing for the government. Given that the banks have been asked to make provisions in their balance sheets relating to risk attached to such assets, their cost (i.e. interest/mark-up) of extending credits and investing in the government securities will automatically increase.

The SBP’s aforementioned action would also have a negative effect on the ability of the banks to extend an unlimited amount of loans and credit to the government – as was in practice before 01 January 2022. Regardless of the prevailing interest rates, the banks would not be able to buy government debt beyond a certain threshold in the new scenario.

Consequently, it would be more expensive for the government to contract loans, or to issue bonds and sovereign paper. This will add further burden to already unsustainable debt-servicing. It will also jack up the currently high budget deficit.

Furthermore, the stature and ratings of government credit and sovereign securities would take a hit. These financial assets may no longer attract creditors and investors in the same manner as before this change.

The change is a clear signal to the financial markets that the government’s domestic obligations carry the risk of default and therefore these financial assets would lose their attraction, despite being sovereign.

This development will also have an impact on the pricing of our external borrowing: once a country’s risk is established on domestic debt, it will have a natural bearing on the pricing of Pakistan’s foreign-currency-denominated sovereign debt. Recently Pakistan’s Sukuk has been priced at 7.95 percent, as opposed to US-benchmark interest rate of 1.73 percent. This is the highest ever profit rate on a Sukuk floated by the country.

Conclusion

It is intriguing that no reaction from the Ministry of Finance has been seen on such a major change by the SBP in public policy. This appears to be a decision taken by the SBP in pursuance of the so-called “central bank autonomy” granted by Imran Khan’s cabinet through the approval of an amendment Bill to the State Bank of Pakistan Act 1956 – a measure that is being widely debated in the country.

The way in which the PTI government has bulldozed its way past objections to the SBP Amendment Bill 2021 in the National Assembly, as well as the unprofessional and hurried manner in which it was passed last Friday in the Senate of Pakistan, speaks volumes of how little this government cares for the financial sovereignty of Pakistan.

The enforcement of IFRS-9 with effect from 01 January 2022 has also strangely coincided with the prohibition – through amendment in the SBP law – on the Federal Government from borrowing from its own central bank. Keeping in view the serious ongoing financial crisis faced by the government, the above discussed action of the SBP is nothing but a serious, unwarranted hit on the financial sovereignty of Pakistan.

In other words, the SBP has advised the banks to start taking into account the probability of default on sovereign loans taken by the Government and, as a result, to make adequate provision in their financial statements for the potential loss on such sovereign lending.

A belief that the government cannot default on domestic debt has been virtually buried.

Pakistan’s history on sovereign obligations

Since its inception in August 1947, Pakistan has never defaulted on any of its domestic debt/obligations. Furthermore, barring the 1971 separation of East Pakistan, when a small default occurred on Official Bilateral Debt, Pakistan has not ever defaulted on its external debt. With such a long history of performance, it is curious as to why the SBP has chosen to require the banks to make provisions for holding Pak-rupee-denominated credit and securities of the Federal Government.

It is incomprehensible to suggest that the Government of Pakistan, a sovereign state capable of printing its currency, would ever fail to fulfill its Pak-rupee-denominated debt servicing obligations. Therefore, it makes no sense to deprive government loans and securities from the status of “risk-free” sovereign financial assets.

What could the rationale be?

The SBP has not given any rationale for the said change.

The best explanation is the need to enforce IFRS-9. However, given that government loans and securities were exempted until 31 December 2021, there has to be some basis for withdrawal of such exemption.

This development will also have an impact on the pricing of our external borrowing: once a country’s risk is established on domestic debt, it will have a natural bearing on the pricing of Pakistan’s foreign-currency-denominated sovereign debt

This is a serious matter and the SBP should have consulted the Government of Pakistan before taking such a far-reaching step.

What are the effects?

The foremost implication of excluding government loans and sovereign securities from the status of “risk-free financial assets” is an increase in the cost of borrowing for the government. Given that the banks have been asked to make provisions in their balance sheets relating to risk attached to such assets, their cost (i.e. interest/mark-up) of extending credits and investing in the government securities will automatically increase.

The SBP’s aforementioned action would also have a negative effect on the ability of the banks to extend an unlimited amount of loans and credit to the government – as was in practice before 01 January 2022. Regardless of the prevailing interest rates, the banks would not be able to buy government debt beyond a certain threshold in the new scenario.

Consequently, it would be more expensive for the government to contract loans, or to issue bonds and sovereign paper. This will add further burden to already unsustainable debt-servicing. It will also jack up the currently high budget deficit.

Furthermore, the stature and ratings of government credit and sovereign securities would take a hit. These financial assets may no longer attract creditors and investors in the same manner as before this change.

The change is a clear signal to the financial markets that the government’s domestic obligations carry the risk of default and therefore these financial assets would lose their attraction, despite being sovereign.

This development will also have an impact on the pricing of our external borrowing: once a country’s risk is established on domestic debt, it will have a natural bearing on the pricing of Pakistan’s foreign-currency-denominated sovereign debt. Recently Pakistan’s Sukuk has been priced at 7.95 percent, as opposed to US-benchmark interest rate of 1.73 percent. This is the highest ever profit rate on a Sukuk floated by the country.

Conclusion

It is intriguing that no reaction from the Ministry of Finance has been seen on such a major change by the SBP in public policy. This appears to be a decision taken by the SBP in pursuance of the so-called “central bank autonomy” granted by Imran Khan’s cabinet through the approval of an amendment Bill to the State Bank of Pakistan Act 1956 – a measure that is being widely debated in the country.

The way in which the PTI government has bulldozed its way past objections to the SBP Amendment Bill 2021 in the National Assembly, as well as the unprofessional and hurried manner in which it was passed last Friday in the Senate of Pakistan, speaks volumes of how little this government cares for the financial sovereignty of Pakistan.

The enforcement of IFRS-9 with effect from 01 January 2022 has also strangely coincided with the prohibition – through amendment in the SBP law – on the Federal Government from borrowing from its own central bank. Keeping in view the serious ongoing financial crisis faced by the government, the above discussed action of the SBP is nothing but a serious, unwarranted hit on the financial sovereignty of Pakistan.